Back to blog

Business Tax Deductions Explained: 2026 Guide

Discover what is business tax deduction and how to reduce your tax bill. Our 2026 guide simplifies the process for small business owners.

Discover what is business tax deduction and how to reduce your tax bill. Our 2026 guide simplifies the process for small business owners.

A business tax deduction is an IRS-allowed expense you subtract from your gross business income to reduce the amount of income the government taxes. The formal term is “ordinary and necessary business expense,” defined by the IRS as any cost that is common in your industry and helpful to running your business. Understanding what is business tax deduction means understanding how to legally shrink your tax bill before you calculate what you owe. Tools like IRS Schedule C and bookkeeping services like Taxbowl make this process manageable for small business owners who want to keep more of what they earn.

A business tax deduction lowers your taxable income by allowing you to subtract ordinary and necessary expenses paid while carrying on a business. This is the IRS baseline rule, and it applies to sole proprietors, partnerships, S-corps, and C-corps alike. If your business earns $100,000 and you have $30,000 in qualified deductions, you only pay taxes on $70,000. That difference is real money back in your business.

The IRS defines “ordinary” as an expense that is common and accepted in your trade or industry. “Necessary” means the expense is helpful and appropriate for your business, even if it is not strictly required. A freelance graphic designer paying for Adobe Creative Cloud meets both tests. A restaurant owner buying kitchen equipment meets both tests. A consultant paying for a home office meets both tests, provided the space is used exclusively for business.

Not every expense qualifies. Personal costs mixed with business costs must be separated. If you use your car 60% for business and 40% for personal trips, only 60% of the car-related costs are deductible. The IRS expects you to track this split and document it clearly. Mixing personal and business spending is one of the most common reasons deductions get disallowed during an audit.

Business expenses must be both ordinary, meaning common and accepted in your industry, and necessary, meaning helpful and appropriate to your business operations. This two-part test is the foundation of every deduction claim you make. Pass both tests, and the expense is deductible. Fail either one, and the IRS can reject it.

Here are the most widely applicable categories of qualifying expenses for small businesses:

The line between personal and business expenses is where most small business owners run into trouble. Buying a new laptop for your business is deductible. Buying one for your child’s schoolwork is not. If you use the laptop for both, you can only deduct the business-use percentage.

Documenting every expense at the time it occurs is the most reliable way to protect your deductions. Save receipts, note the business purpose, and record who was present for any meal or entertainment expense. A simple spreadsheet works, but accounting software makes this far easier to maintain consistently.

Pro Tip: Set a weekly 15-minute block to categorize and log expenses. Doing this in real time prevents the year-end scramble that causes missed deductions and filing errors.

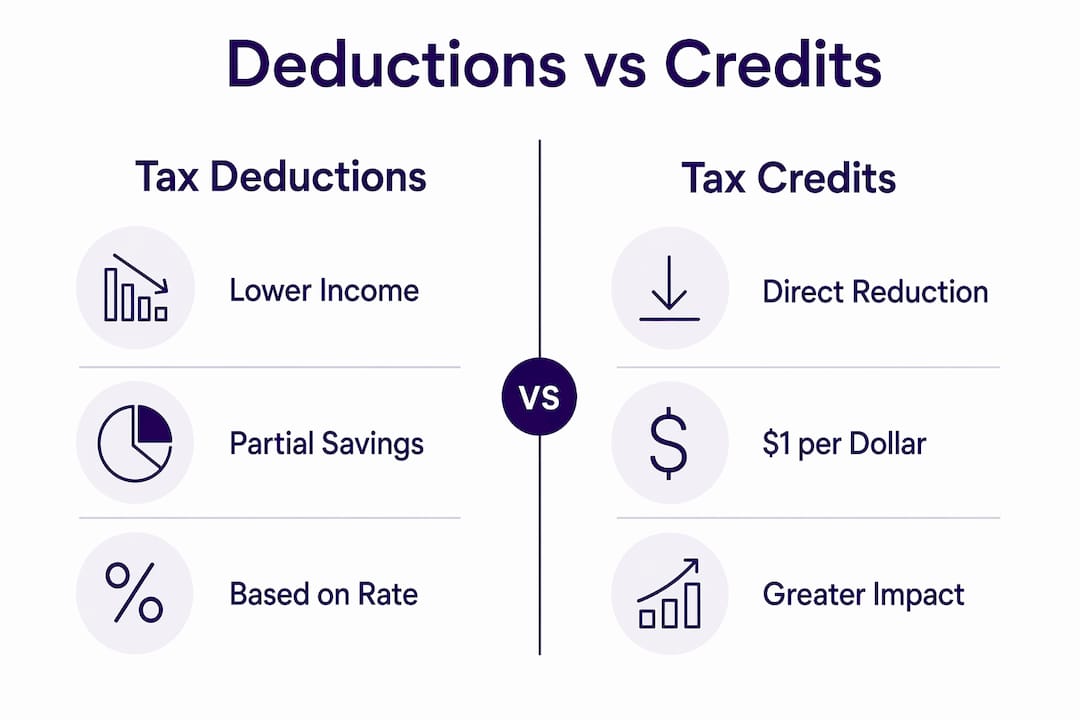

Deductions lower taxable income, while tax credits reduce the actual tax you owe, dollar for dollar. This distinction matters more than most business owners realize. A $1,000 deduction does not save you $1,000 in taxes. It saves you $1,000 multiplied by your marginal tax rate.

Here is a side-by-side comparison to make this concrete:

| Scenario | Deduction | Tax Credit |

|---|---|---|

| Amount | $5,000 | $5,000 |

| Marginal tax rate | 22% | 22% |

| Actual tax savings | $1,100 | $5,000 |

| How it works | Reduces taxable income | Reduces tax owed directly |

| Example | Home office deduction | Small Business Health Care Tax Credit |

The table shows why credits generally provide more direct tax savings than deductions. That said, deductions are far more widely available and easier to qualify for. Credits often come with strict eligibility requirements, income limits, or specific industry conditions.

Your marginal tax rate determines how much a deduction is actually worth to you. If you are in the 24% bracket, every $1,000 in deductions saves you $240. If you are in the 32% bracket, that same $1,000 saves you $320. Higher earners get more value from each deduction, which is why tax planning matters more as your business grows.

Small businesses can access credits like the Work Opportunity Tax Credit, the Small Business Health Care Tax Credit, and the Disabled Access Credit. These are worth pursuing alongside your standard deductions. The two strategies work together, not in competition.

Pro Tip: Claim every deduction you qualify for first, then layer in any credits. Deductions reduce the income base that credits are calculated against, so the order of operations affects your final tax bill.

NerdWallet identifies home office, supplies, software, insurance, rent, utilities, advertising, travel, meals, and professional fees as the core categories of small business tax deductions aligned with Schedule C. These are the deductions most small business owners can access without complex eligibility requirements. Knowing them in detail helps you avoid leaving money on the table.

The IRS offers a simplified method for the home office deduction: $5 per square foot up to 300 square feet, for a maximum deduction of $1,500. You do not need to track actual home expenses like mortgage interest or utilities under this method. The space must be used regularly and exclusively for business. A dedicated room qualifies. A kitchen table where you occasionally work does not.

The 2026 IRS standard mileage rate is $0.725 per mile driven for business purposes. If you drive 10,000 miles for business in 2026, your deduction is $7,250. You must keep a mileage log with dates, destinations, and business purposes. Apps like MileIQ or Everlance automate this tracking and generate IRS-compliant reports.

Expenses deducted on Schedule C reduce the business’s profit or loss, which flows directly to your adjusted gross income on Form 1040. This makes business deductions “above-the-line,” meaning they reduce your AGI before you even calculate your standard or itemized deductions. For sole proprietors, this is one of the most powerful tax tools available.

Tracking expenses weekly and maintaining receipts throughout the year reduces the risk of disallowed deductions during filing. The IRS does not accept estimates. Every deduction you claim must be supported by documentation that shows the amount, date, vendor, and business purpose of the expense. Building this habit early in the year makes tax season far less stressful.

Here is a practical process for claiming deductions accurately:

Common mistakes to avoid include deducting personal expenses as business costs, failing to document the business purpose of meals and travel, and missing the home office deduction because the rules seem complicated. Each of these errors either leaves money unclaimed or creates liability if the IRS questions your return.

Pro Tip: Set up a monthly financial review with your bookkeeper or accountant, not just an annual one. Proactive management throughout the year means you capture every deduction and avoid scrambling to reconstruct records in april.

Claiming every eligible business deduction requires consistent documentation, a clear understanding of IRS rules, and the right tools to track expenses throughout the year.

| Point | Details |

|---|---|

| Core definition | A business tax deduction subtracts qualifying expenses from taxable income, reducing the taxes you owe. |

| IRS eligibility test | Expenses must be both ordinary (common in your industry) and necessary (helpful to your business) to qualify. |

| Deductions vs. credits | Deductions reduce taxable income; credits reduce tax owed dollar for dollar and generally deliver more direct savings. |

| Top 2026 deductions | Home office ($1,500 max simplified), mileage ($0.725/mile), health premiums, retirement contributions, and software all qualify. |

| Documentation is non-negotiable | Weekly expense tracking, digital receipts, and monthly reconciliation protect your deductions if the IRS asks questions. |

Most small business owners treat tax deductions as a year-end task. That single habit costs them more money than any missed deduction category ever could. By the time december arrives, receipts are gone, expense categories are blurry, and the home office calculation feels like guesswork. The owners who consistently pay less in taxes are not finding secret deductions. They are tracking the obvious ones all year long.

The most overlooked deductions I see are retirement contributions and health insurance premiums. Both are fully deductible for self-employed owners, both reduce AGI directly, and both get skipped because owners assume they are too complicated. A SEP-IRA contribution of $10,000 at a 24% tax rate saves $2,400. That is not a rounding error. That is a real return on a decision you were already making for your future.

Tax rules also change. The 2026 mileage rate, the Section 179 limits, and the rules around bonus depreciation are not the same as they were three years ago. Staying current matters. I recommend reviewing IRS updates each january and confirming your deduction strategy with a professional before you file, not after.

The businesses that grow fastest are the ones where the owner is not buried in financial admin. Delegating bookkeeping to a service like Taxbowl frees you to focus on revenue while someone else makes sure every deductible dollar is captured. That is not an expense. That professional fee is itself a deduction.

— Taxbowl

Running a business is demanding enough without spending hours categorizing expenses and second-guessing IRS rules.

Taxbowl’s bookkeeping services are built specifically for small businesses and entrepreneurs who want accurate financials without the administrative burden. The Taxbowl team tracks your deductible expenses in real time, reconciles your accounts monthly, and gives you clear visibility into your financial position throughout the year. With an average of $53,399 in outstanding receivables identified for clients, Taxbowl delivers the kind of financial clarity that prevents costly mistakes. When tax season arrives, your records are clean, your deductions are documented, and your filing is straightforward. Connect with the Taxbowl team to see how professional bookkeeping pays for itself in tax savings alone.

A business tax deduction is an expense the IRS lets you subtract from your business income before calculating the taxes you owe. The more qualified deductions you claim, the lower your taxable income and your tax bill.

Common business tax write-offs include rent, utilities, supplies, software, insurance, advertising, mileage, professional fees, health insurance premiums, and retirement contributions. Each expense must be ordinary and necessary to your business to qualify.

Sole proprietors report deductible business expenses on Schedule C, which attaches to Form 1040. The total deductions reduce your net business profit, which lowers your adjusted gross income and the taxes you owe.

A deduction reduces your taxable income, so your savings equal the deduction amount multiplied by your tax rate. A credit reduces your actual tax bill dollar for dollar, making credits generally more valuable when you qualify for them.

Yes. The IRS simplified method allows a deduction of $5 per square foot for up to 300 square feet, capping at $1,500. The space must be used regularly and exclusively for business to qualify.