Back to blog

Quarterly Estimated Tax Payments Guide for 2026

Navigate your tax obligations with our quarterly estimated tax payments guide for 2026. Learn how to calculate, submit, and avoid penalties!

Navigate your tax obligations with our quarterly estimated tax payments guide for 2026. Learn how to calculate, submit, and avoid penalties!

Quarterly estimated tax payments are periodic tax payments self-employed individuals and small business owners must make to cover income and self-employment taxes not withheld from paychecks. The IRS operates on a pay-as-you-go system, which means you owe tax throughout the year, not just at filing time. Miss a payment or underpay, and you face penalties that compound each quarter. This quarterly estimated tax payments guide walks you through who must pay, how to calculate the right amount, where to submit payments, and how to protect your cash flow when income fluctuates.

The IRS requires quarterly estimated tax payments from anyone who expects to owe at least $1,000 in federal tax after subtracting withholdings and credits. Corporations face a lower bar: they must pay if they expect to owe $500 or more. That threshold applies to your total tax liability, not just income tax.

Self-employed individuals and small business owners are the most common group affected. No employer withholds taxes from your revenue, so covering income and self-employment tax falls entirely on you. That includes Social Security and Medicare taxes, which add up to 15.3% of net self-employment income.

State-level rules add another layer. State estimated tax obligations vary by state and sometimes trigger at lower thresholds than federal requirements. California, New York, and Illinois each have their own deadlines and calculation rules. Check your state’s revenue department alongside IRS guidance.

The IRS divides the year into four uneven periods. Each period has a firm deadline. Missing any one of them triggers a penalty calculated from that specific due date forward.

| Quarter | Income Period | Due Date |

|---|---|---|

| Q1 | January 1 – March 31 | April 15, 2026 |

| Q2 | April 1 – May 31 | June 15, 2026 |

| Q3 | June 1 – August 31 | September 15, 2026 |

| Q4 | September 1 – December 31 | January 15, 2027 |

Notice that Q2 covers only two months while Q4 covers four. That uneven structure catches many first-time payers off guard. Plan your cash reserves around these dates, not around calendar quarters.

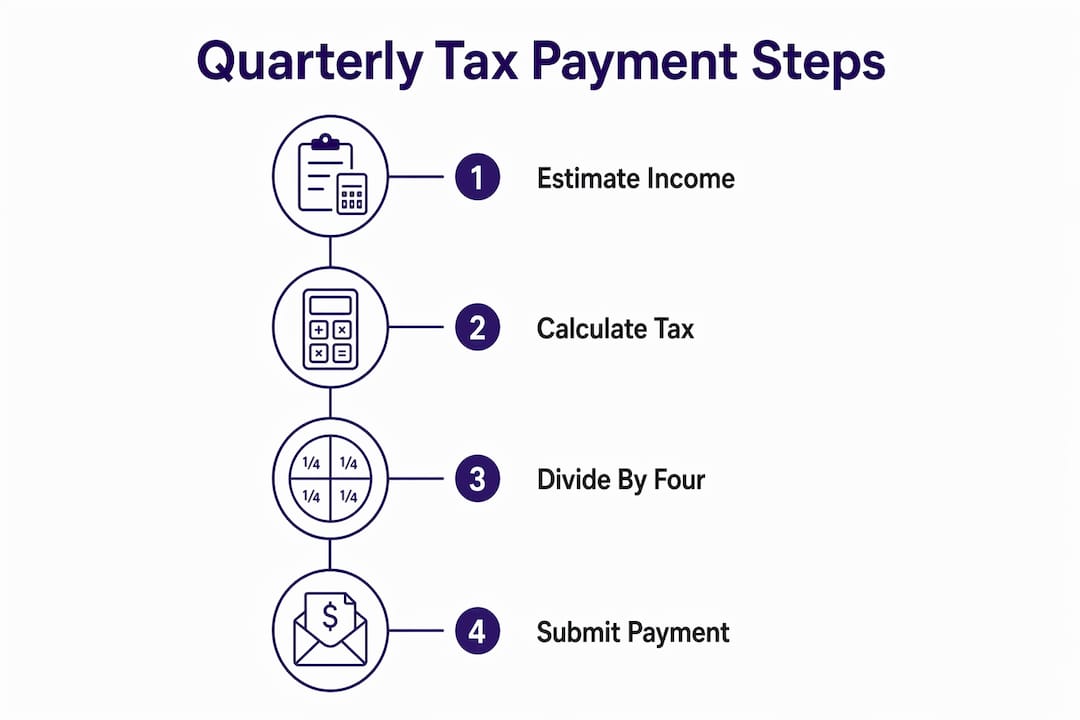

Three calculation methods exist for estimated taxes, and the right one depends on your income stability and how long you have been in business.

The safest and simplest approach is the prior-year safe harbor method. You pay 100% of last year’s total tax liability spread across four equal payments. If your adjusted gross income (AGI) exceeded $150,000 last year, you must pay 110% of last year’s tax to qualify for safe harbor protection. Meeting either threshold means the IRS cannot penalize you for underpayment, even if you end up owing more at filing.

This method works best for established businesses with stable or growing income. The math is straightforward: pull your prior-year Form 1040, find the total tax line, divide by four, and pay that amount each quarter. You may still owe a balance in April, but you avoid penalties entirely.

This method requires you to project your total income and tax liability for the current year. You estimate your net profit, subtract deductions, apply the self-employment tax deduction (50% of SE tax), and calculate what you will owe. Divide that projected annual tax by four and pay equal installments.

Accurate income estimation is critical here. Include federal income tax, self-employment tax, and any applicable state income tax in your calculation. Leaving out self-employment tax is one of the most common mistakes small business owners make. It adds up to a significant amount and surprises many people at filing time.

The IRS Form 1040-ES includes a worksheet that walks you through this calculation step by step. The worksheet accounts for deductions, credits, and self-employment tax adjustments. Use it as your starting point, then update your projection each quarter as your actual income becomes clearer.

The annualized income method is the right tool when your income is seasonal or unpredictable. New business owners without prior-year tax returns benefit most from this approach. It matches your payments to actual cash flow rather than forcing equal installments regardless of what you earned.

Here is how it works in practice. At the end of each quarter, you annualize your actual income to date by multiplying it by the appropriate factor (4 for Q1, 2 for Q2, 1.33 for Q3, and 1 for Q4). You then calculate the tax on that annualized figure and pay the corresponding percentage of that amount. The IRS Form 2210 Schedule AI documents this calculation.

A freelance designer who earns $10,000 in Q1 and $40,000 in Q3 would overpay significantly using equal installments. The annualized method lets that designer pay less in Q1 and more in Q3, matching payments to actual earnings.

Pro Tip: Review your income and expenses at the midpoint of each quarter, not just at the deadline. A mid-quarter check gives you time to adjust your payment before the due date without scrambling.

The IRS offers several payment methods, and each has practical trade-offs worth knowing before you commit to one.

IRS Direct Pay is the fastest option for individuals. You go to IRS.gov, enter your bank account information, and schedule a payment in minutes. No registration required, and you receive immediate confirmation. Direct Pay is free and available 24 hours a day.

EFTPS (Electronic Federal Tax Payment System) has historically been the go-to for businesses. However, the IRS is planning to disable EFTPS for individual quarterly payments in 2026, while continuing it for businesses. If you currently use EFTPS as an individual, verify your options before the April 15 deadline.

The IRS2Go app and IRS online account both support estimated tax payments from a mobile device. The IRS online account also lets you view your payment history and verify that previous payments were applied correctly. That verification step matters more than most people realize.

Mail-in payments using Form 1040-ES vouchers remain an option, but processing times vary. If you mail a check, send it at least 7 to 10 business days before the deadline and keep a copy of the check and the voucher.

Pro Tip: Set a recurring calendar reminder two weeks before each quarterly deadline. That buffer gives you time to calculate your payment, move funds if needed, and submit without rushing.

Variable income is the norm for most small business owners and freelancers. The good news is that the IRS provides clear rules for adjusting your payments without triggering penalties.

The two safe harbor thresholds are your primary protection. First, you can pay 90% of your current year’s expected tax liability across the four quarters. Second, you can pay 100% of last year’s tax liability (or 110% if your prior-year AGI exceeded $150,000). Meeting either threshold means underpayment penalties do not apply, even if you owe a balance at filing.

Here is a numbered process for recalculating mid-year when income shifts significantly:

Overpaying is not a disaster, but it does tie up cash you could use in your business. Underpaying across multiple quarters compounds quickly. Penalties are calculated as interest on the underpaid amount from the due date of the missed payment until you pay it. Each quarter with a shortfall adds to the total.

Consider a concrete example. A marketing consultant projects $80,000 in net income for 2026 but earns $15,000 in Q1 and $55,000 by the end of Q3. After Q3, she recalculates and realizes her annual income will likely hit $90,000. She increases her Q4 payment to cover the gap. Because her cumulative payments through Q3 already met the 90% threshold for the year, she avoids any penalty even though her earlier estimates were low.

Pro Tip: If your income drops sharply in a quarter, do not skip the payment entirely. Pay the lower amount that reflects your actual earnings. A small payment is always better than no payment when it comes to penalty calculations.

The annualized installment method, documented on IRS Form 2210 Schedule AI, is the formal tool for this process. It requires more active tracking than the safe harbor method, but it can be financially advantageous for businesses with seasonal or uneven income streams. A tax professional can help you decide whether the extra calculation effort is worth it for your specific situation.

Managing quarterly estimated taxes correctly protects your cash flow and keeps you clear of IRS penalties throughout the year.

| Point | Details |

|---|---|

| Know your threshold | Individuals owing $1,000 or more must pay quarterly; corporations owe at $500. |

| Mark your deadlines | The four 2026 due dates are April 15, June 15, September 15, and January 15, 2027. |

| Use safe harbor rules | Pay 100% of last year’s tax (110% if AGI exceeded $150,000) to avoid underpayment penalties. |

| Choose the right method | Use the annualized income method when revenue is seasonal or unpredictable. |

| Track every payment | Record the date, amount, method, and confirmation number for each quarterly payment. |

Most small business owners do not miss quarterly payments because they are careless. They miss them because no one told them the deadlines were uneven, or that self-employment tax had to be included in the calculation, or that state payments run on a separate schedule entirely. The system is not designed to be intuitive.

What I have seen consistently is that the owners who stay on top of estimated taxes are not necessarily the ones with the most financial knowledge. They are the ones who built a simple system early. A dedicated tax savings account, a calendar with the four deadlines, and a quarterly income review. That is the whole system. It does not require sophisticated software or a finance degree.

The calculation method matters more than most guides admit. The safe harbor method is fine for stable businesses, but it can cause real cash flow strain for a seasonal business that overpays in Q1 and Q2. The annualized method takes more work, but it keeps your payments aligned with what you actually earned. Choosing the wrong method is not a penalty risk, but it is a cash flow risk.

State taxes are the most overlooked piece. I have worked with business owners who paid their federal estimates perfectly and then received a state underpayment notice they did not expect. State estimated tax obligations have their own thresholds and deadlines. Treating them as an afterthought is a costly habit.

The broader point is this: good tax habits and good financial habits are the same habits. When you know your numbers, review them regularly, and pay on time, you are also building the kind of financial visibility that helps you make better business decisions year-round.

— Taxbowl

Staying compliant with quarterly estimated taxes is easier when your books are clean and your numbers are current. Taxbowl’s bookkeeping services for growing businesses keep your income and expenses organized in real time, so you always have accurate figures when it is time to calculate your next payment.

Taxbowl pairs a dedicated team of accountants with proactive communication through platforms like Slack, so you get timely answers instead of waiting until tax season. With an average cash visibility of $53,399 in outstanding receivables tracked for clients, Taxbowl gives you the financial clarity to make confident decisions. If you want expert support for your small business accounting and tax needs, Taxbowl is built for exactly that.

Estimated quarterly tax is a prepayment of income and self-employment taxes made four times per year to the IRS. It applies to self-employed individuals and business owners whose taxes are not withheld by an employer.

You must pay quarterly estimated taxes if you expect to owe at least $1,000 in federal tax after withholdings and credits for the year. Corporations face a $500 threshold.

The prior-year safe harbor method is the most reliable approach. Pay 100% of last year’s total tax liability across four equal payments, or 110% if your prior-year AGI exceeded $150,000.

The IRS calculates a penalty as interest on the underpaid amount from the due date of the missed payment forward. Each quarter with a shortfall adds to the total penalty, making timely payments critical.

Yes, you can pay more frequently than quarterly to manage cash flow. The IRS only evaluates cumulative payments by each quarterly deadline when determining whether a penalty applies.