Back to blog

Why Manual Bookkeeping Fails Small Business Owners

Discover why manual bookkeeping fails small business owners, where errors and compliance gaps appear, and how modern tools improve financial accuracy.

Discover why manual bookkeeping fails small business owners, where errors and compliance gaps appear, and how modern tools improve financial accuracy.

Manual bookkeeping is defined as the practice of recording financial transactions by hand or in disconnected spreadsheets, and it fails small businesses because it is structurally prone to human error, IRS compliance gaps, and reconciliation breakdowns that compound over time. The core problem is not effort or intention. It is that manual processes cannot keep pace with the accuracy, speed, and documentation standards that modern financial management demands. Tools like QuickBooks exist precisely because spreadsheet-based accounting creates the kinds of errors that cost small businesses real money. Understanding why manual bookkeeping fails is the first step toward fixing it.

Reconciliation is where manual bookkeeping most visibly breaks down. QuickBooks reconciliation guidance identifies the most common culprits as uncleared transactions, missing entries, duplicate records, and bank statements that combine multiple payments into a single line item. Each of these issues is easy to miss in a manual system and hard to trace once the month closes.

The real danger is timing. Your books may show a payment as cleared while the bank has not yet processed it. Or your bank combines three vendor payments into one deposit, and your spreadsheet records them separately. These mismatches do not cancel out. They accumulate, and by quarter-end you are chasing discrepancies that could take hours to untangle.

Here are the most common reconciliation failures in manual bookkeeping:

Pro Tip: Apply the same matching logic every single month. Consistency in how you match bank entries to book records matters more than math precision. One month of inconsistent logic creates a reconciliation problem that takes three months to diagnose.

The most common reconciliation failures trace back to gaps in transaction entry or timing differences with bank reporting, not calculation errors. That distinction matters because no amount of double-checking your math fixes a structural matching problem.

The IRS does not accept good intentions as documentation. Under IRC §274(d), business expenses for meals, travel, and vehicle use require what the IRS calls “adequate records,” meaning contemporaneous documentation that captures the amount, date, location, business purpose, and the business relationship of anyone involved. A receipt alone is not sufficient.

This is where manual bookkeeping creates serious audit risk. Most small business owners keep receipts in a folder or photograph them sporadically. What they rarely do is annotate each receipt with the specific business purpose at the time of the expense. The IRS requires that detail to be recorded contemporaneously, meaning at or near the time of the transaction, not reconstructed months later during tax prep.

The consequences of failing this standard are concrete:

“Failure to maintain detailed contemporaneous business purpose on receipts leads to disallowed deductions under IRS rules despite having receipts.” — IRS Receipt Requirements: The Complete Business Guide

Manual systems make contemporaneous documentation harder because there is no automatic prompt to add context when an expense is entered. Digital tools with receipt capture and memo fields solve this by design. Manual systems require discipline that most business owners, understandably focused on running their companies, do not consistently apply.

Human error in manual bookkeeping is not random. It is predictable, and it compounds. Small mistakes build into inaccurate financial data that distorts your profit picture, triggers compliance risks, and leads to poor decisions about hiring, spending, and growth. The problem is not that people make mistakes. The problem is that manual systems have no early warning mechanism to catch them.

Consider the operational sequence when an error occurs in a spreadsheet-based system:

Beyond errors, manual processes lack role-based controls and audit trails, which creates real fraud vulnerability. When one person handles data entry, payment approval, and reconciliation, there is no separation of duties. Fraud in small businesses is disproportionately committed by trusted employees precisely because manual systems offer no structural check on their access.

Annual manual bookkeeping costs average $10,000 to $25,000 for small and mid-sized firms when you account for time lost, error correction, and compliance risks. That figure does not include the opportunity cost of hours you spend on data entry instead of sales, client work, or strategy.

Pro Tip: If one person in your business handles both transaction entry and bank reconciliation, you have a separation-of-duties gap. Even a simple second-person review of monthly reconciliations reduces fraud risk significantly.

Manual bookkeeping does not scale. As your transaction volume grows, the time required to maintain accurate records grows at the same rate, or faster. Increased transaction complexity forces more manual effort or forces compromises in data quality. Neither outcome supports a growing business.

The scalability gap becomes a compliance gap when regulators, lenders, or investors ask for clean, auditable records. A business preparing for a bank loan, an investor review, or a state audit needs records that are complete, consistent, and traceable. Manual systems rarely produce that without significant cleanup work.

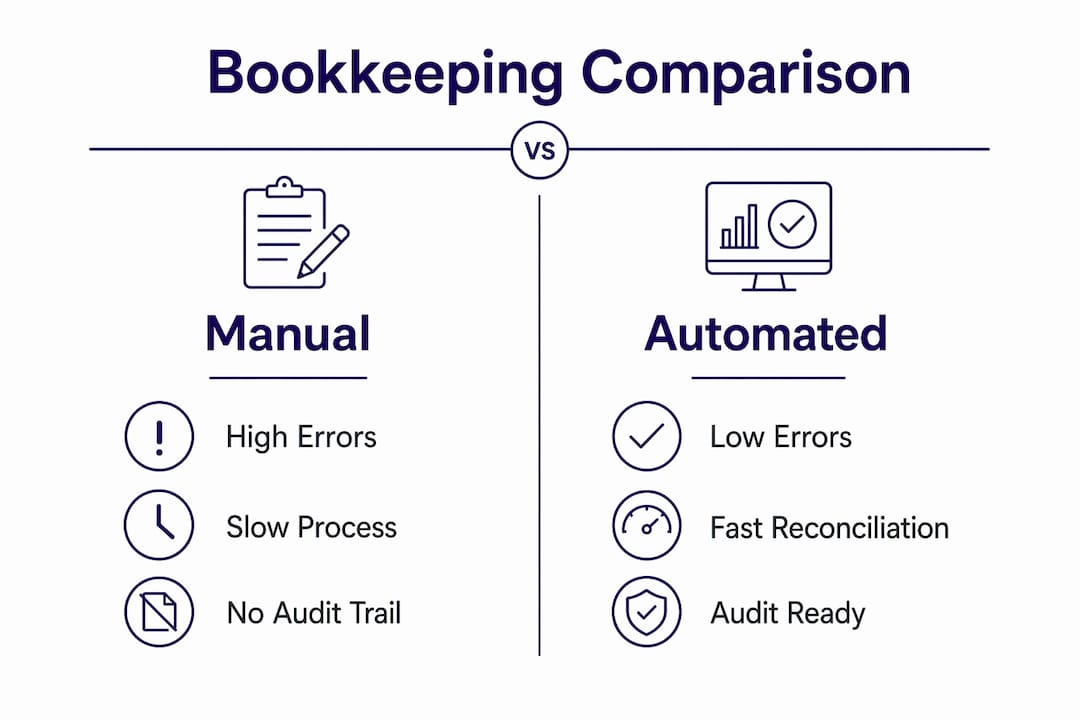

Here is a direct comparison of how manual and automated bookkeeping perform as a business grows:

| Factor | Manual bookkeeping | Automated bookkeeping |

|---|---|---|

| Error rate as volume grows | Increases proportionally | Stays low with rule-based matching |

| Time per transaction | Fixed or increases | Decreases with automation |

| Audit trail quality | Inconsistent, hard to trace | Complete and timestamped |

| IRS compliance readiness | Reactive, often incomplete | Proactive, documentation built in |

| Monthly close time | Days to weeks | Hours |

| Cost at scale | Linear increase in staff time | Marginal cost stays flat |

Automation reduces reconciliation time by 75% and cuts errors by over 90%. That is not a marginal improvement. It is a structural shift in how financial data gets produced and how reliably it can be trusted.

For businesses navigating compliance and formation requirements, the gap between manual and automated recordkeeping becomes even more consequential when regulators expect digitally linked, audit-ready documentation.

Fixing the challenges of manual bookkeeping does not require an overnight overhaul. It requires a deliberate sequence of changes that reduce error exposure and build toward audit-ready records.

Pro Tip: Set a recurring calendar block on the last business day of each month for reconciliation. Treating it as a fixed appointment, not a task you get to when time allows, is the single habit that prevents most year-end bookkeeping disasters.

The benefits of digital bookkeeping go beyond accuracy. Real-time financial visibility lets you make faster decisions on cash flow, hiring, and vendor payments. That visibility is simply not available from a spreadsheet updated weekly or monthly.

Manual bookkeeping fails small businesses because its structural weaknesses in reconciliation, IRS compliance, fraud prevention, and scalability create compounding financial and legal risks that grow faster than the business itself.

| Point | Details |

|---|---|

| Reconciliation is the first failure point | Uncleared checks, duplicate entries, and combined bank payments break manual matching logic every month. |

| IRS rules demand more than receipts | IRC §274(d) requires contemporaneous business purpose notes; receipts alone do not protect your deductions. |

| Human error compounds over time | Small entry mistakes flow into reports, tax filings, and audits before most owners notice them. |

| Manual systems do not scale | As transaction volume grows, error rates and staff time increase proportionally with no efficiency gain. |

| Automation delivers measurable ROI | Digital bookkeeping cuts reconciliation time by 75% and errors by over 90%, with average ROI of 150 to 300%. |

Here is what I have observed working with small business owners over many years: most do not switch away from manual bookkeeping because it is failing them. They switch because it has already failed them, usually during a tax filing, a loan application, or an IRS inquiry. By that point, the cleanup cost is three to five times what prevention would have cost.

The misconception I hear most often is that manual bookkeeping is “good enough for now” and that automation is something to consider once the business grows. That logic is backwards. The time to build accurate financial systems is before complexity arrives, not after. A business with 50 monthly transactions can set up clean automated bookkeeping in a weekend. A business with 500 monthly transactions and two years of messy spreadsheets needs weeks of professional cleanup.

The other pattern I see is owners who know their books are inaccurate but avoid looking closely because the process of fixing it feels overwhelming. That avoidance is expensive. Every month of delayed reconciliation adds to the backlog. Every unannoted receipt is a deduction at risk. The IRS does not grade on effort.

The practical advice I give every time: start with one change. Connect your bank feed to accounting software this week. Reconcile this month’s statement before the next one arrives. Document the business purpose on your next three receipts. Small, consistent steps break the cycle faster than waiting for the perfect moment to overhaul everything at once.

— GroupJDC

If this article has surfaced problems you recognize in your own books, you are not alone. Most small business owners reach a point where manual processes cost more in time, errors, and missed deductions than professional help would.

Taxbowl’s bookkeeping and accounting services are built specifically for startups and small businesses that need accurate, audit-ready financials without the overhead of a full in-house accounting team. Taxbowl combines a dedicated team of accountants with real-time financial visibility and direct communication via Slack, so you get answers when you need them, not at the end of the quarter. With an average of $53,399 in outstanding receivables tracked per client, Taxbowl gives you the cash flow clarity that manual systems simply cannot provide. If you are ready to stop managing your books reactively, explore Taxbowl’s services and see what proactive financial management looks like in practice.

Manual bookkeeping fails because it relies on human consistency for accuracy, lacks early error detection, and cannot meet IRS substantiation standards for documentation. These weaknesses compound over time into reconciliation gaps, compliance risks, and distorted financial reports.

Under IRC §274(d), the IRS requires contemporaneous records with specific business purpose notes for meals, travel, and vehicle expenses. Manual systems rarely capture this detail at the time of the expense, leading to disallowed deductions even when receipts exist.

Annual manual bookkeeping costs average $10,000 to $25,000 for small and mid-sized firms when accounting for time lost, error correction, and compliance exposure. Automated systems typically deliver 150 to 300% ROI by comparison.

Manual bookkeeping requires hand entry and human matching of every transaction, while automated bookkeeping uses bank feeds and rule-based logic to import and categorize transactions automatically. Automation reduces reconciliation time by 75% and errors by over 90%.

The right time to move away from manual bookkeeping is before transaction volume exceeds what you can reconcile accurately in a few hours per month. Once errors start appearing in your reports or reconciliation takes more than a day, the cost of professional or automated bookkeeping is already justified.